On May 11, Anthropic issued a notice that rattled secondary share markets for some of the highest-valued private companies in technology. The company declared that any transfer of its stock through an unauthorized party is void, named eight platforms whose offerings it considers prohibited, and banned special purpose vehicles as a vehicle for gaining economic exposure to its equity. The aftermath was swift: funds claiming Anthropic exposure shed a third or more of their value within days, and investor chatrooms from London to Seoul spent the week processing what the notice actually means.

The crackdown was not entirely without precedent. Private companies routinely include transfer restrictions in their charter documents, and enforcing them against specific secondary platforms is a known tool. What was unusual was the breadth of Anthropic's notice, its specificity about prohibited structures, and its timing, which arrived just as secondary valuations on Anthropic shares were touching implied figures close to $1 trillion.

What Anthropic Said

Anthropic's statement, published on its support page, is specific about what it prohibits. The list covers direct sales of its stock to unapproved buyers, beneficial interests in its shares, forward contracts referencing its equity, special purpose vehicles, and tokenized products. Both preferred and common stock are covered, and any transfer not approved in advance by Anthropic's board of directors is void, regardless of when it occurred or which platform facilitated it.

The notice named eight firms by name: Open Doors Partners, Unicorns Exchange, Pachamama Capital, Lionheart Ventures, Hiive (new offerings only), Forge Global (new offerings only), Sydecar, and Upmarket. The carve-out for "new offerings" on Hiive and Forge Global, both established secondary-market platforms, suggests Anthropic is targeting the expansion of secondary activity rather than attempting to retroactively void all legacy trades on those particular venues.

Anthropic's Secondary Market Crackdown: Key Facts

- Notice dateMay 11, 2026

- Prohibited structuresSPVs, forward contracts, tokenized products, beneficial interests

- Named platforms8, including Hiive and Forge Global (new offerings)

- Secondary-market implied valuation before notice~$1 trillion

- Tokenized Anthropic PreStocks decline34–38%

- Affected closed-end fund decline~25%

The Market Impact

Secondary markets for AI company shares had been growing quickly, and Anthropic's trajectory had made it one of the most actively traded names. At the time of the notice, Solana-based tokenized instruments referenced to Anthropic's implied share price were trading at levels consistent with a company valuation approaching $1 trillion. The effect of the voiding notice was immediate: tokenized Anthropic PreStocks fell roughly 34 to 38 percent in the days that followed, while similar instruments linked to OpenAI, which issued a comparable notice around the same period, dropped around 39 to 46 percent.

"Any offer or sale of Anthropic shares through any vehicle not authorized in advance by Anthropic's board of directors is void." Anthropic support page, May 2026

Publicly traded closed-end funds with claimed Anthropic exposure also took substantial losses. Sohail Prasad, whose fund was among the most visible, contested the validity of Anthropic's claims publicly, arguing on X that his fund's holdings predated the relevant transfer restrictions and should be treated as legitimate equity. The legal question of whether a private company can unilaterally void completed secondary transfers through a notice posted on its website is not settled, and several affected parties are expected to pursue the matter in court.

Why Now

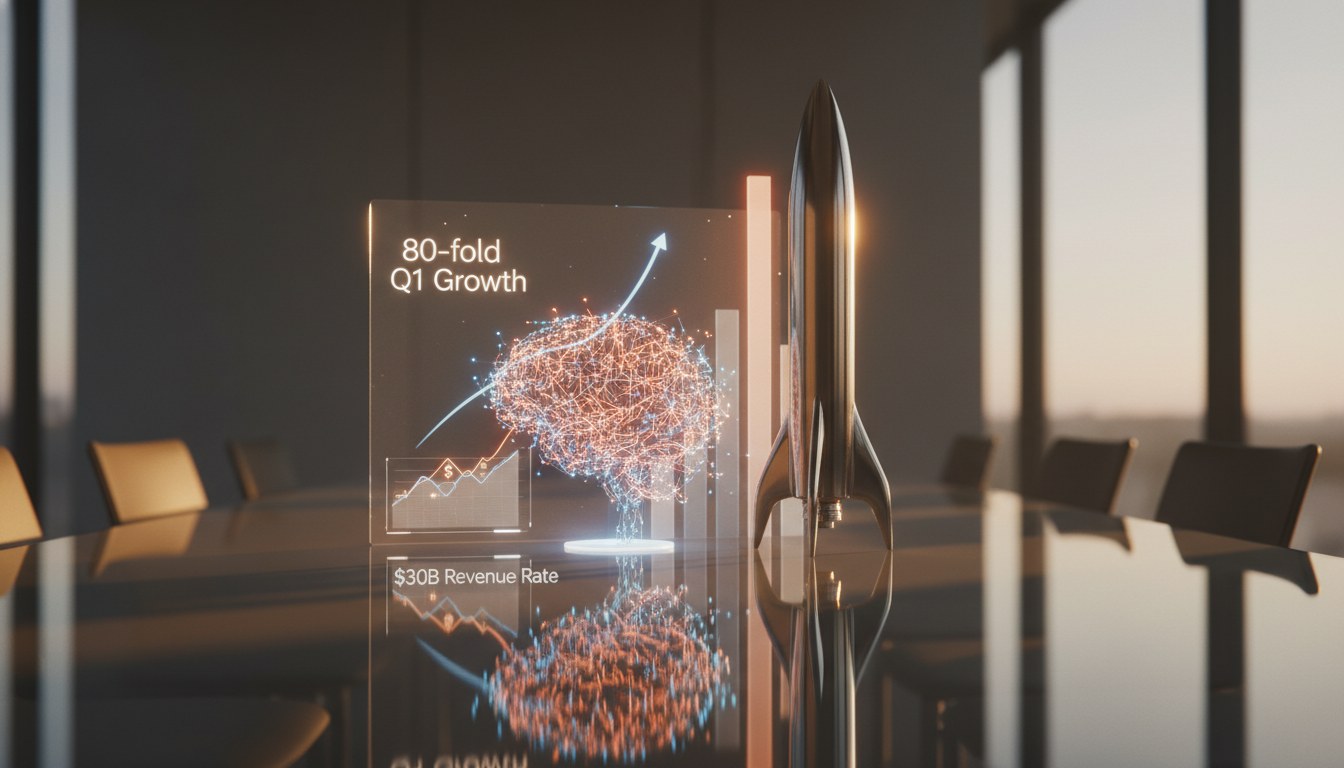

Anthropic has strong reasons to want tight control over its equity at this stage. The company reported 80-fold revenue growth in the first quarter of 2026, reaching a $30 billion annualized run rate. It is simultaneously in discussions for a funding round that could push its valuation toward $950 billion. At those numbers, the gap between the company's internally sanctioned valuation and whatever the secondary market implies becomes a material concern for the primary-round negotiation. Unauthorized secondary markets set unofficial pricing benchmarks that can complicate the terms of a new institutional round.

There are regulatory dimensions as well. Private companies face restrictions on the number of shareholders of record, and secondary-market structures, particularly SPVs that pool multiple retail investors, can push a company toward thresholds that trigger mandatory public registration under U.S. securities law. Anthropic has not cited this as a motivation, but it is a standard consideration for private companies with active secondary markets and investor bases of this size.

What Comes Next for Secondary Buyers

For retail investors who purchased secondary-market instruments before the notice, the path forward is unclear. Those who hold tokenized products will need to assess whether to pursue legal remedies, attempt to liquidate through whatever thin liquidity remains, or hold positions and hope that a future IPO or liquidity event resolves the ownership question in their favor. For institutions that built positions through SPVs, the legal exposure is more direct: if Anthropic's voiding argument is upheld, the vehicles may have no underlying asset to distribute to their investors.

The broader lesson for pre-IPO secondary markets is harder to avoid. Platforms in this space had benefited from years in which major technology issuers often tolerated unauthorized secondary trading, particularly when high valuations attracted willing buyers and the issuer preferred a quiet status quo. Anthropic's action, and OpenAI's parallel notice, signals that tolerance is ending for the most visible AI companies, at least during the final private stages before any liquidity event. Whether that pressure spreads to secondary markets in other private companies depends partly on what happens in any litigation that follows, and partly on whether other issuers view Anthropic's approach as a template worth replicating.

Anthropic itself has not commented on IPO timing. The company's founders have consistently framed Anthropic's mission as a long-horizon safety project rather than a path to a public listing on any particular schedule. But the secondary market's implied trillion-dollar valuation, and the company's decision to actively police unauthorized trading at that level, suggests the question is becoming harder to defer indefinitely.